Permanent Tax Brackets Solidified

For years, taxpayers, accountants, and business owners had a calendar date circled in red: December 31, 2025.

T. Brown

8/8/20254 min read

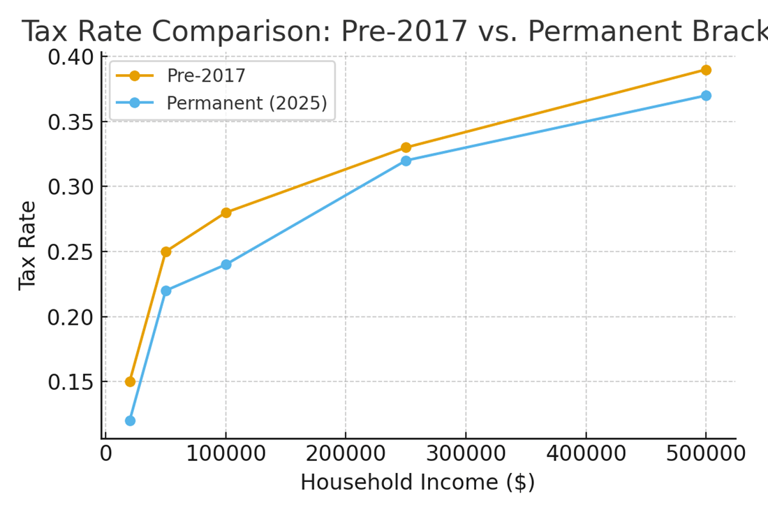

For years, taxpayers, accountants, and business owners had a calendar date circled in red: December 31, 2025. That was when the individual tax rate cuts from the 2017 Tax Cuts and Jobs Act (TCJA) were set to expire. If Congress had done nothing, millions of households would have seen their tax bills rise in 2026 as rates reverted to higher pre‑2017 levels. In 2025, lawmakers finally made their move. The seven‑bracket system—10%, 12%, 22%, 24%, 32%, 35%, and 37%—was made permanent.

This development is more than just an update to a chart. It’s a policy signal that Congress favors stability over uncertainty. Families and businesses now know that, absent new legislation, the basic framework of rates will not change in 2026. For planners and everyday workers alike, that clarity matters.

What Changed

Before this change, the lower brackets created in 2017 were set to sunset. That would have meant, for example, the 12% bracket reverting to 15%, the 22% bracket rising to 25%, and so on. The permanence of today’s brackets means the tax landscape looks the same in 2026 as it does in 2025.

Source: PerspectiveTax - 2025

Write your text hereReal‑World Examples

Middle‑income family: A household earning $95,000 falls in the 22% bracket. Without permanence, that same family would have faced a 25% rate in 2026, raising their tax bill by over $2,800. Permanence keeps their tax planning consistent.

High earners: A couple earning $600,000 remains in the 37% bracket. Their liability doesn’t change compared with 2024, but they avoid the uncertainty of higher potential rates.

Business owners: Pass‑through income taxed at individual rates now has predictability. Owners can make investment decisions without worrying about sudden bracket jumps.

Pros

Stability: Families and companies can plan for savings, retirement, and investments without worrying about bracket jumps.

Political clarity: Removes a recurring debate that created anxiety every budget season.

Administrative simplicity: The IRS, payroll departments, and software providers avoid costly recalibrations.

Cons

Revenue cost: Keeping rates lower than pre‑2017 levels means less money flowing into the Treasury, which could increase deficits.

Distribution: The benefit of permanency skews toward higher earners, who save the most in dollar terms from lower top rates.

Temporary elsewhere: Other TCJA provisions, like the expanded Child Tax Credit, still sunset, leaving a patchwork of temporary and permanent rules.

Why It Matters

In tax policy, uncertainty is often as damaging as high rates. When families and business owners don’t know what rules will apply next year, they hold back on decisions—delaying investments, slowing hiring, or saving less. Permanence takes that cloud away. For example, financial planners advising retirees on Roth conversions can now model outcomes with more confidence. Similarly, businesses weighing equipment purchases know their marginal tax rates won’t suddenly rise after 2025.

On the political side, making brackets permanent reflects a compromise: low‑ and middle‑income taxpayers gain peace of mind, while top earners continue to face the highest rate of 37%. It’s not perfect, but it is predictable.

Ultimately, permanence of the brackets helps Americans focus on managing their finances instead of second‑guessing Congress. That stability is valuable in its own right.

Key Takeaway:

Making the seven tax brackets permanent eliminates uncertainty and allows families and businesses to plan confidently for the future.

Opinion: Permanent Tax Brackets – Stability or Giveaway?

The 2025 decision to make the seven federal income tax brackets permanent was hailed as a win for stability. No more uncertainty about whether rates would revert in 2026 to pre-TCJA levels. For planners, businesses, and households, that’s reassuring. But in my view, the permanence of these brackets is a mixed bag—one that tilts benefits toward the wealthy while providing only modest comfort to middle-class families.

First, the good. Predictability matters. A family deciding whether to convert a traditional IRA to a Roth now knows exactly what tax rate applies to that conversion. Business owners considering equipment purchases or expansion no longer face the cloud of higher future brackets. In finance, certainty has a real value.

But let’s look at who really wins. A household earning $90,000 will still pay roughly the same as before. The permanence saves them maybe a few hundred dollars compared with pre-2017 rules. By contrast, a couple earning $500,000 saves tens of thousands per year by locking in today’s 35% and 37% rates instead of reverting to 39.6%. That’s a huge windfall for those at the top, and it comes at the cost of federal revenue.

The deficit problem is real. Making lower rates permanent reduces the Treasury’s intake by hundreds of billions over a decade. Unless spending is cut—a politically unlikely scenario—that gap fuels more borrowing. In effect, we’re handing a long-term tax cut to the affluent and sending the bill to future taxpayers.

Another subtle problem is that permanence in brackets doesn’t mean permanence across the whole tax code. Credits like the expanded Child Tax Credit still expire. Some deductions phase in and out. So while the rate structure is stable, the rest of the code remains a patchwork. Families may feel like they have certainty when in fact major parts of their tax picture remain unsettled.

My opinion: Congress missed an opportunity. If they were going to make changes permanent, they should have paired bracket permanence with broader family-focused reforms. Imagine making the Child Tax Credit permanent too, or ensuring the Earned Income Tax Credit automatically adjusts with cost of living. That would have given middle- and lower-income households more genuine stability.

Instead, permanence largely functions as a victory for higher earners and their lobbyists. For everyone else, it’s a mixed blessing—welcome clarity, but not the kind of tax fairness that actually levels the playing field. Policymakers should revisit this choice with an eye toward balance, not just predictability.

Citation

U.S. Bank. “2025 Federal Income Tax Brackets.” U.S. Bank. https://www.usbank.com/wealth-management/insights/2025-federal-income-tax-brackets.html...