OBBBA Senior Deduction ($6,000)

When we talk about tax laws, the language can feel dry and disconnected from daily life. But for millions of seniors living on fixed incomes, even modest changes can ripple through their budgets in meaningful ways.

T. Brown

6/10/20254 min read

The One Big Beautiful Bill Act (OBBBA) of 2025 introduced such a change: a brand‑new $6,000 standard deduction specifically for Americans age 65 and older. Unlike many targeted provisions, this one is straightforward—if you’re 65 or older, you qualify. No complicated forms, no tricky income phase‑outs at the start. It’s a simple subtraction from your taxable income that can free up cash for essentials.

To show how this works in practice, let’s look at a real‑world case study.

Case Study: Alice’s Story

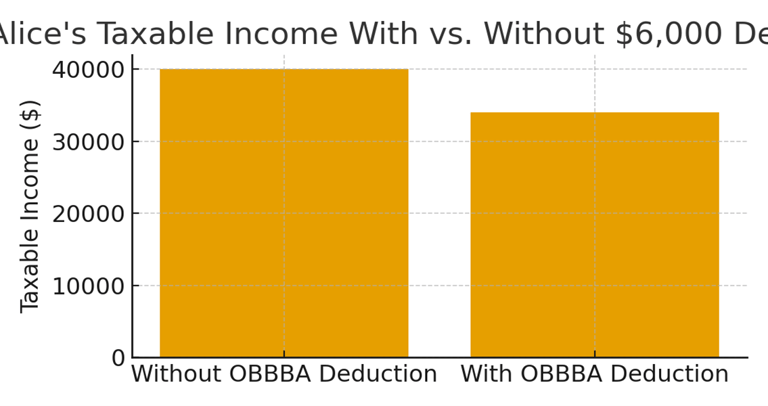

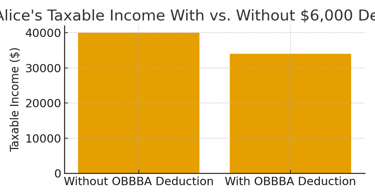

Alice is 70 years old and lives in a modest apartment in Ohio. She receives about $25,000 in Social Security benefits each year, plus $15,000 from a small pension. In total, her annual income is $40,000. Like many retirees, her budget is tight—rent, groceries, medications, and utility bills consume nearly all of her monthly check.

Before 2025, Alice’s taxable income was $40,000 (minus her regular standard deduction). Starting this year, she gets an additional $6,000 deduction. That drops her taxable income to $34,000. At a 12% tax rate, her tax bill shrinks by about $720. That may not sound like much to some households, but for Alice, $720 covers three months of electric bills or more than a year’s worth of prescription co‑pays.

Source: PerspectiveTax - 2025

Broader Impacts

Alice’s example shows how the OBBBA deduction provides immediate, tangible relief. Multiply her story by millions of seniors, and the policy’s significance becomes clear. Retirees often have little flexibility in their budgets; an unexpected tax bill can mean skipping medications, delaying a needed repair, or cutting back on food. By lowering taxable income automatically, the $6,000 deduction creates breathing room without requiring seniors to navigate complicated eligibility tests.

The deduction also levels the playing field. Higher‑income retirees often have access to accountants, financial planners, and strategies to reduce taxable income. Lower‑ and middle‑income seniors like Alice usually do not. This deduction gives them a straightforward benefit that doesn’t depend on complex planning.

There are limitations. The deduction begins to phase out for retirees with very high incomes, ensuring the biggest benefits flow to those who need them most. And unless Congress acts, the deduction expires in 2028. For seniors hoping to count on it long‑term, that creates uncertainty.

Pros

Provides automatic tax relief to seniors with no extra paperwork.

Targets relief where it’s most needed—those on fixed incomes.

Offers meaningful, if modest, annual savings that compound over time.

Cons

Temporary measure—set to expire in 2028 unless extended.

Phase‑outs reduce impact for higher‑income retirees.

May not be enough to offset steep increases in healthcare or housing costs.

Why It Matters

Tax policy can sometimes feel like abstract math, but the OBBBA deduction highlights the human side of tax law. For Alice, it’s not about percentages or formulas—it’s about whether she can pay her bills without stress. For policymakers, it’s a recognition that seniors face unique financial pressures, especially as they live longer and rely on fixed incomes.

This deduction also sparks conversations about how tax policy should support aging populations. As America’s demographics shift, more households will depend on Social Security and modest pensions. Small but broad benefits like the OBBBA deduction could become a model for future reforms.

Key Takeaway:

The $6,000 OBBBA senior deduction turns abstract policy into real relief, helping retirees like Alice stretch limited incomes further.

Opinion: The Senior Deduction – Fair Relief or Missed Opportunity?

The OBBBA’s introduction of a $6,000 standard deduction for seniors over 65 made headlines for its simplicity and generosity. If you’re 65 or older, you get to knock $6,000 off your taxable income, no questions asked. For retirees like Alice, the woman in our earlier case study, that’s hundreds in tax savings every year. On the surface, it looks like smart, compassionate policy. But in my opinion, the deduction is both a step forward and a missed opportunity.

First, the positives. Simplicity matters. Too many tax breaks come with strings attached—income thresholds, phase-outs, paperwork hurdles. The senior deduction avoids all that. It acknowledges that older Americans face unique financial pressures and gives them relief in a way that doesn’t require an accountant. That’s a genuine win.

But here’s where I think it falls short: seniors aren’t the only group struggling. Millennials and Gen Z face skyrocketing housing costs, student loan payments, and medical debt. Many are raising families while caring for aging parents at the same time. In focusing relief solely on seniors, Congress left out millions of taxpayers in equally precarious situations.

There’s also the matter of fairness across income levels. A senior with $200,000 in retirement income still gets the same $6,000 deduction as a senior scraping by on Social Security alone. That means the benefit disproportionately helps those who arguably need it least. A more targeted credit—say, one that phased out for higher incomes—would have directed resources where they’re most impactful.

Lastly, the deduction is temporary. Unless extended, it sunsets in 2028. That undercuts the stability seniors crave in retirement planning. Imagine adjusting your budget around annual tax savings only to lose them three years later. Policymakers should either commit to making it permanent or pair it with broader reforms to Social Security and Medicare that more directly address seniors’ long-term security.

In my view, the senior deduction is a political gesture—valuable to those who receive it, but incomplete as policy. If Congress truly wants to honor and support older Americans, it should design benefits that are permanent, progressive, and paired with relief for younger generations carrying the heaviest financial loads.

Citation

Investopedia. “This New Senior Tax Break Could Lower Your Taxes: How to Know if You Qualify.” Investopedia, 2025. https://www.investopedia.com/new-senior-tax-break-2025-obbba-7501234